W3PG: Blockchain Technology

Blockchain technology is the underlying architecture that powers the crypto space.

by

Ondre

Last updated on 5/25/2021

Learn about what powers Web 3

Welcome to your next lesson!

After the primer on decentralization you should have a better understanding of the differences between decentralized and centralized networks. Or, you can go back and read it again! Ha.

Decentralization is important to understand because it disrupts the current network and systems we find ourselves in today. But decentralized networks would not be possible without blockchain technology. This piece will be aimed at giving you a high-level overview so that you can understand what all the hype is about!

To understand blockchain technology we will take a look at it’s history, functionality, and mechanisms through real-world use cases. The paradigm-shifting technology that has enabled networks like Bitcoin and Ethereum is relatively new but packs a lot of promise for the future. Let’s jump into the beginning!

Without blockchain technology, software such as Bitcoin and Ethereum could not exist. The technology is new and fresh. It’s also the foundation for dapps and DeFi. To kick off the article let’s give a brief history of blockchain technology and how it emerged.

Satoshi, Bitcoin and Blockchain

The concept of blockchain can be dated back to the early 90s. But it didn’t get its claim to fame until 2008, when a person or group of people under the pseudonym Satoshi Nakomoto released a series of white papers for Bitcoin. In this mysterious release, a breakthrough electronic cash system was established and just like that, the blockchain revolution was born.

Nakomoto’s goal was not only to eliminate the need of third parties, but to provide a tighter and more secure method of transactions and payments. After the financial crisis of 2008, Satoshi saw that incompetent third parties could no longer be entrusted with the world’s economics. To solve this dilemma, Nakomoto invented bitcoin. Through Bitcoin, problems that led to the current financial crisis such as double spending (a currency that can be spent twice) were fixed. But ultimately, a new king of technology that would transcend beyond payments was established.

Satoshi created the first successful use case for blockchain technology. It’s important to note that bitcoin and blockchain are mutually exclusive. Bitcoin is the currency used to transact within the network and blockchain is the technological infrastructure that enables these transactions to occur.

Bitcoin played an important role in introducing a successful use case for blockchain technology. It allowed users to electronically send money over the internet in peer-to-peer transactions without needing intermediaries or institutions like banks. Aside from paving the way for a digital currency, it showed that there is a new and verifiably safe way to transact over the internet.

Blockchain: the Distributed Ledger

Hold up! Do you know what a ledger is? And did you know that we use them everyday? If not, here’s a quick definition: ledgers are tracking systems that keep record of financial transactions. Transactions like debt, credit, payments, etc, are all kept in ledgers.

Blockchain technology is a form of a distributed ledger, which is a database that every node in a network has access to. These ledgers are shared and synchronized across multiple sites and can be accessed by anyone since they are public. This provides a new level of transparency that effectively minimizes shady behavior, while at the same time offering security. It’s a win-win!

Most companies use centralized ledgers to keep track of important data, assets and finances. We are accustomed to these centralized systems because they have typically been our sole option. Blockchain, which is a distributed ledger, takes a different approach and makes this info public and tamper-proof. It omits human mistakes and provides us with attributes that we take for granted like financial freedom/control, anonymity, and improved security.

Financial Control:

- Bitcoin allows full autonomy over who, where and when people can send their money

- There is no gatekeeping intermediary to tell you how much you can send, when to send it, or who you can send it to

- Blockchain provides access to all financial transaction history in the network

Privacy and Anonymity:

- When two parties engage in a transaction, both the receiver and sender receive a public and private key

- Public and private keys are encrypted and decrypted bits of data that signify and represent a transaction

- Public keys decrypt data and are open source so everyone in the network can see it

- Private keys encrypt data and are for personal use only (hidden from public)

- Both private and public keys permit anonymity, concealing the real identity of both parties, while simultaneously identifying transaction history on the blockchain

Security:

- Cryptocurrencies, like bitcoin, require wallets that come with special codes so the individuals who own them have personal access

- Hardware wallets hook up to computers and store cryptocurrencies on physical storage

- Software wallets store cryptocurrency digitally and are password-protected

- Prevents hackers from breaching into accounts and stealing funds

- Blockchain technology makes transactions irreversible and immutable, preventing people from manipulating information

Blockchain and its properties are far more valuable than storing and recording information. For some demographics, blockchain represents a new tool. One that allows access to necessitous things, such as funds. Outside of the States, there are legitimate use cases for blockchain technology that are being worked on in real time. When thinking of blockchain, it’s easy to get lost in how disruptive it is. It can easily be romanticized. But with the romantic beliefs aside, how many of us really think about the actual problems it can solve with humanity? We’re barely seeing the creativity and innovation that blockchain can produce.

How Blockchains Work

To fully grasp blockchain technology, one must learn the components of it. What comprises blockchains are: blocks, miners, and nodes. Without these elements, blockchains would malfunction. Each element plays a key role in how data is stored, how information is distributed, and how consensus is achieved. Let’s break them down, piece by piece, in order to comprehend how it all works.

Blocks

A blockchain is a series of blocks that are linked together. Sounds obvious, right? Each block contains a hash value, or a signature of data that is uniquely represented. When one block is completed, another one forms and connects itself to the last one, and so on and so forth. That way every node in the network has access to the data and information in the blockchain. The data inside the blocks are immutable (non-erasable), irreversible, and permanent. That way data and information is protected against corrupt and fraudulent activity.

Miners

Miners are responsible for solving complex math problems, using loads of computational power, which adds bitcoin into circulation. By solving these math problems, new blocks are verified and submitted onto the blockchain. Once miners complete and verify transactions, they receive some cryptocurrency, such as bitcoin, for their problem solving. This process of solving and verifying transactions is called Proof-of-Work (PoW). Proof-of-Work helps secure the blocks in the blockchain, since it runs on a consensus mechanism. There’s no third party or overseer to ensure each block is verifiable and securable. And since blockchains are decentralized and require consensus, someone has to maintain the health and validity of the blockchain.

Nodes

Nodes refer to computers, laptops, or other servers that are hooked up to the blockchain. Nodes are interconnected to one another and make up the infrastructure of the blockchain. They have a copy of each transaction and hold data stored on-chain. Since most blockchains are open source peer-to-peer networks, nodes are free to directly communicate and send information between each other. When the nodes verify the transactions, they use cryptography to identify the digital signature, or hash, to confirm the signature is identical to the code. Hence where crypto comes from!

Nodes are important because they ensure that the blocks verified by miners are valid, that way they can properly secure and store transaction history from the blocks completed by miners. The difference between miners and nodes is that nodes are copies of transaction history, while miners are workers who verify those transactions.

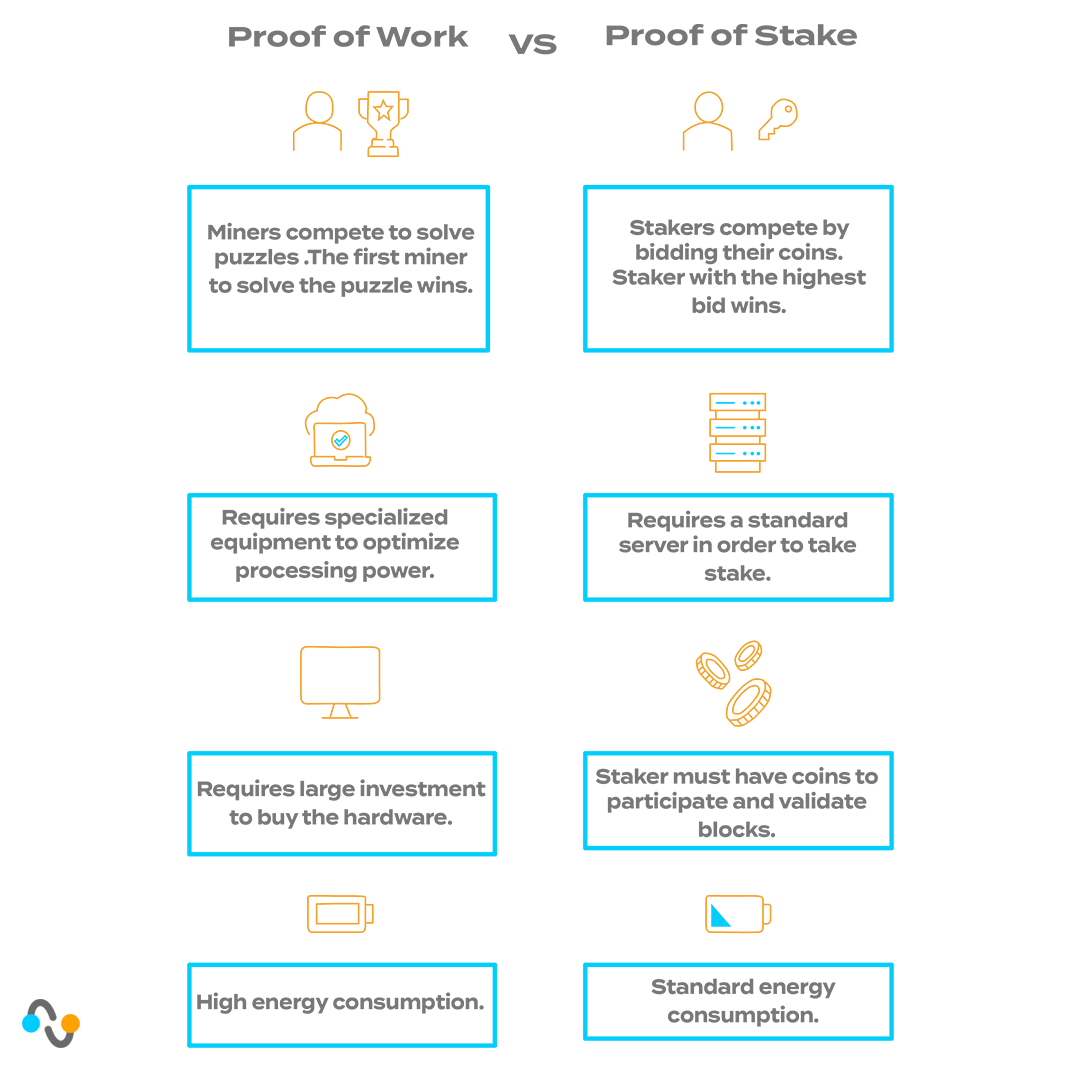

Proof of Work vs Proof of Stake

In order for blocks to be added and verified to the blockchain, a consensus mechanism must be put in place. There are a few ways to reach consensus. The first method is proof of work, where miners solve mathematical equations, or puzzles, with specific hardware and computer power in order to validate blocks on the blockchain. The other way is proof of stake, where people bid their own coins to validate blocks.

Proof of work is when miners solve complex mathematical equations, or puzzles, in order to verify a block. To solve these puzzles, one doesn’t need as much skill as much as they need lots of computational power. With miners around the globe all competing to complete a transaction, the ones with the most hardware and computational power tend to win the most. The puzzles on bitcoin’s protocol come periodically, and typically block generation occurs in a 10 minute interval. This can be inefficient and congest the blockchain, especially if lots of transactions are occurring at once.

Proof of stake looks to solve the scalability and congestion issues that the Bitcoin, and even Ethereum, protocols endure. Instead of competing to solve mathematical puzzles, proof of stake systems use coins to determine and validate blocks. To give you an example, let’s say one person has 10 coins and the other person has 50 coins. The person staking 50 coins is more likely to validate the next block than the person with 10 coins. The higher the stake, the more likely it is that person will validate. And in comparison to proof of work, those in a proof of stake system own the coins they’re staking, which means no new coins are created in the process.

The major differences between proof of work and proof of stake lies in the cost and energy. Compared to proof of work, proof of stake is much cleaner, more cost efficient, and less competitive because proof of stake requires a stake in coins. Competition still exists between stakers, but it’s less costly due to miners having to upgrade equipment and computer power. All stakers need is an x amount of coins to validate. Mining slows transactions down, since miners have to work and use up lots of energy in order to create new coins. Transactions are sluggish and take too much time. In proof of stake, the process is smoother, quicker, and less exhaustive.

Evolution of Blockchains

100 years ago we started driving gas cars; now, autonomous battery-powered cars drive us. 25 years ago we got the web; now the autonomous web is run by us. As technology accelerates, knowledge increases, and humans become increasingly digital: the improved autonomy that we as a species experience mirrors that of the web.

Satoshi set the tone with Bitcoin and has challenged modern financial systems with its public ledger that addresses fraud, corrupt actors and centralized authority in a novel way. Its ability to track, record and store data would eventually lead to the second generation of blockchain technology: smart contracts.

Ethereum pioneered a new use case for blockchains, transitioning from Bitcoin’s vision for a global decentralized financial system into a vision of a decentralized global computer. Creators of Ethereum stepped up the technology, adding on top of the ability to track documents. Smart contracts allow for functionality and programmability within a decentralized environment like Bitcoin’s. In our Decentralization piece (have you read it?), we briefly mentioned smart contracts and their function. But in case you need a refresher, let’s go over it really quick!

Smart contracts are self-executing agreements represented in on-chain code. The parties involved set the agreements or operate according to the agreements already established in the software and the software is able to non-arbitrarily enforce it. For example: if James wants to send Tom ETH (Ethereum’s native currency) for some shoes that Tom agreed to sell, James will write in the code that once he gets the shoes from Tom, then an x amount of ETH will be sent to Tom. Why smart contracts are so important is the same reason Bitcoin is: it removes the middleman and promotes a peer-to-peer network. Typically, conventional contracts require more than two parties. And usually another party is there to oversee the contract, which they can manipulate and include themselves in.

As the generations pass, the new ones try to improve upon the old. None are perfect, nor better than the other. However, each generation focuses on improving core inefficiencies within the blockchain space like scalability. Both Bitcoin and Ethereum have issues to scaling currently. Ethereum acknowledges their flaws, so they created a new version called Ethereum 2.0 to fix the problem of high gas fees. Gas fees are transaction fees paid to miners for completing transactions, which make it difficult for a high amount of transactions to occur on the blockchain. To paint a picture, let’s imagine a startup has a large pie. At first, there’s a lot for everybody. Then as the startup expands, bringing on more people, it grows in size. That’s good for the startup, but not everyone will be able to eat the pie.

So, in the third generation of blockchain technology, blockchains such as Cardano, Solana and Flow look to solve the scalability issues. Different approaches such as side-chains, multi-node architecture and new consensus mechanisms are all approaches towards building better solutions in space. While out of the scope for this piece, these changes are all very exciting and promising for blockchain’s maturity in tech.

Looking Onward

So you got to the end of this article, eh? Well, we’re glad. If you read all this, and still feel confused, don’t stress. It takes a while for this information to seep in until you actually understand it. Hopefully it opens your eyes to the endless new possibilities that blockchain technology creates.

Blockchain technology is dense and definitely not an easy concept to learn. After reading this though, hopefully you get a better idea of the impact that this technology will have on our world! The web allowed the world to connect to each other, now blockchain has allowed us to safely transact with one another. As we integrate the chain into our lives, more creativity will be unlocked, manifesting a more equitable increase in innovation and prosperity.

Thank you for reading.